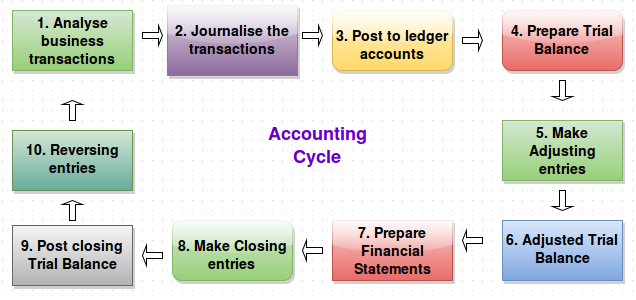

ACCOUNTING TERMINOLOGY

Before we proceed with our study of accounting, we need to learn about some important accounting terms used universally. This will help you in the accounting vocation as well as help you in understanding special meanings attached to these words used in context of accounting.

1. Assets:

The valuable things owned by the business are known as assets. These are the properties owned by the business. Assets are classified as under -

• Fixed assets: These assets are acquired for long term use in the business. They are not meant for resale. Land and Buildings, plant and machinery, vehicles and furniture etc., are some of the examples of fixed assets.

• Current/Liquid assets: These also known as circulating, fluctuating, or current assets. These assets can be converted into cash as early as possible. Current assets are cash, bank balance, debtors, stock, investments, etc.

• Fictitious Assets: Fictitious assets are those assets, which do not have physical form. They do not have any real value. Ex. Loss on issue of shares, preliminary expenses, etc.,

• Intangible assets: Intangible assets are those having no physical existence. Ex. Goodwill, Patents, Trademarks, etc.,

• Wasting Assets: Wasting assets are those assets which are consumed through being worked or used. Mines are the examples of wasting assets.

2. Capital:

It is that part of wealth which is used for further

production and thus capital consists of all current assets and fixed assets.

Cash in hand, cash at bank, buildings, plant and furniture etc., are the

capital of the business. Capital is classified as fixed capital and working

capital.

· Fixed capital: The amount invested in acquiring

fixed assets is called fixed capital. Plant and machinery, vehicles, furniture and buildings etc., are some of the examples for fixed capital.

·

Working capital: The part of capital available with

the firm for day-to-day working of the business is known as working capital.

Working capital can also be expressed as under.

Working

capital = Current assets – Current Liabilities

3. Liabilities:

Liabilities are the obligations or debts payable by

the enterprise in future in the form of money or goods. Liabilities can be

classified as fixed, current and contingent liabilities.

·

Fixed liability: These liabilities are payable

generally, after a long period. Capital, loans, debentures, mortgage etc., are

its examples.

·

Current Liabilities: Liabilities payable within a year

are termed as current liabilities. The value of these liabilities goes on

changing. Creditors, bills payable and outstanding expenses etc., are current

liabilities.

·

Contingent liabilities: These are not the real liabilities.

Future events can only decide whether it is really a liability or not. Due to

their uncertainty, these liabilities are termed as contingent (doubtful)

liabilities.

4. Transactions: Any sale or purchase of goods or services is called

the transaction. Transactions are of three types.

·

Cash transaction: Cash transaction is one where cash

receipt or payment is involved in the exchange

·

Credit transaction: Credit transaction will not have

cash, either received or paid, for something given or received, respectively.

Credit transactions give rise to debtor and creditor relationship.

·

Non- Cash transaction: It is a transaction where the

question of receipt or payment of cash does not arise at all. Ex: Depreciation,

return of goods etc.,

5. Account: Account is the most important entity of an accounting

system, created to group financial transactions having common character.

Simply, a summarized statement of transaction, relating to a particular person,

thing, expense or income called an account.

6. Ledger: A Ledger is a book where various accounts are maintained.

7. Debit: The term debit conveys receiving

aspect of a transaction. For example, when Stationery purchased, we debit

Stationery.

8. Credit: The term credit conveys giving

aspect of a transaction. For example, when Stationery purchased, we pay cash.

Thus we credit Cash.

9. Balance: The difference of sum of debits and sum of credits is

called Balance. It sum of debits is greater than sum of credits, the balance is

called debit balance. If sum of credits is greater than sum of debits, the

balance is called credit balance.

10. Proprietor: Proprietor is a person, who owns the business. He

invests capital in the business with the object of earning profits. Proprietor

is an individual in case of sole trading partner in case of partnership firms

and shareholder in case of companies.

11. Drawings: Cash or goods withdrawn by the proprietor from business

for his personal or household use is termed as ‘drawings’.

12. Solvent: A solvent is a person who is able to pay one’s debts when

they become due.

13. Insolvent: An Insolvent is a person who is unable to pay his debts

when they become due. The condition in which the liabilities exceed the assets.

14. Debtors: A debtor is a person who owes money to the trader.

15. Creditors: A creditor is a person to whom something is owed by the

business. He is a person to whom some amount is payable for loan taken,

services obtained or goods bought.

16. Equity: A claim which can be enforced against the assets of a firm

is called equity. The equities of the firm are two types – Owners equity or

capital and Creditors equity.

17. Goods: All those things which a firm purchases for resale are

called goods.

18. Purchases: Purchases means purchase of goods, unless it is stated

otherwise. It also represents the goods purchased.

19. Sales: Sales means sale of goods, unless it is stated otherwise. It

also represents the goods sold.

20. Revenue: Revenue in accounting means the amount realized or

receivable from the sale of goods.

21. Expenses: Payments for the purchase of goods or services are known

as expenses. It is the cost of use of things or services for the purpose of

generating revenue.

·

Capital expenditure: If the benefits of

expenditure are expected to accure for a long time, that expenditure is called

capital expenditure.

Ex:

Cost furniture, cost of machinery, etc.,

·

Revenue expenditure: Expenditure which is

incurred by the trader in the course of his business and in maintaining an

asset in proper condition is known as Revenue expenditure.

Ex:

Salaries, Rent, Taxes, insurance, etc.,

·

Deferred revenue expenditure: When huge amount of expenditure is incurred in one

year and the corresponding benefits are likely to be received over a number of

years it is known as deferred revenue expenditure.

Ex:

Advertisement expenses arose over five years

22. Income: It is the amount earned by the

business entity resulting operations which constitutes its major activities. Ex:

Sale

·

Capital Income

or Capital profit: If any asset is sold more than its book value, the

excess amount realized is treated as a capital gain.

·

Revenue

Income: Revenue income means an income which arises out of and in

the course of the regular business transactions of a concern.

23. Discount: Discount is two types – Cash discount and Trade discount

·

Cash

discount: An allowance made to encourage prompt payment or before the

expiration of the period allowed for credit

·

Trade

discount: A deduction from the gross or catalogue price allowed to traders who

buys them for resale.

24. Voucher: Accounting transaction must be supported by documents.

These documentary proofs in support of the transactions are termed as vouchers.

25. Narration: It describes the details of a transaction, such as Party

or person who transacting, purpose of expense or income and duration covered by

the transaction. For example, Salaries paid for the month of ….. .

26. Reserve: An amount set aside out of profits or other surplus and

designed to meet contingencies.

27. Accounting period: A

period of 12 months for which the accounts are usually kept. It may be calendar

year (January 1st to December 31st) or financial year

(April 1st to March 31st)

28. Profit and Loss account: It is a statement prepared by the

businessman for the ascertainment of profit or loss during the accounting

period.

29. Losses: It is to be distinguished from expense. An expense s

supposed to bring some benefit to the firm, whereas a loss will not. Loss by

fire or theft is an example.

30. Gross profit: The

difference between the selling price and the cost price of goods, before the

deduction of any expenses incurred in selling goods.

31. Net profit: The profit

that remains after deducting all the expenses from the gross profit. It

represents the real gain of the business.

32. Balance sheet: It is a

statement of assets and liabilities prepared with a view to measure the exact

financial position of a business on a particular date, generally the last date

of the accounting period.

33. Accounting equation:

Assets = Capital + Liabilities

34. Trial Balance: It is a statement containing the balances of all

ledger account at any given date.

35. Cheque: A cheque is a bill of exchange

drawn on specified banker and not expressed to be payable otherwise than on

demand. Simply, a cheque is a demand on a banker.

36. Bad debts: It is an irrecoverable

amount from Sundry debtors.

37. Opening stock: It represents the stock

of goods with the trader at the commencement of the trading period.

38. Customers: Customers are persons, who

purchased goods from us on credit basis.

39. Suppliers: Suppliers are persons, who

sold goods to us on credit basis.