INTRODUCTION TO ACCOUNTING

Commerce started with ‘Barter’ system of trade in which goods and services were exchanged for goods and services. So there was no need of accounting as every transaction was settled at the time exchange of goods or services only. The people of that time didn’t require recording the transactions. But when they started trade with cash and transactions in the trade were increased, they required recording the transactions in a proper manner.

Accounting came into existence to record business transaction in a systematic way. Early records of accounts were more of recording transactions in terms of Receipts and Payments. With introduction of Double Entry system of Book keeping by Fraetr Luca Paciolo in 1494, the accounting is universally employed.

Accounting and Book Keeping:

Accounting is the process of recording, classifying and summarizing business transactions in a systematic manner and deals in interpreting the results.

The day – to – day record keeping of business transaction is called Book Keeping. Book Keeping systems are two types. They are Single entry system of Book keeping and Double Entry system of Book keeping.

Double Entry System:

The double entry system of book keeping is recognized as the most scientific system of book keeping. Every business transaction involves a transfer and as such consists of two aspects namely, receiving aspect and giving aspect. It is impossible to think one without other. The recording of any business transaction can not be completed unless the two aspects of the transaction are recorded. For example, while purchasing goods, business concern receives goods and gives cash in return. Thus the basic principle of double entry system is that for every debit there must be corresponding credit.

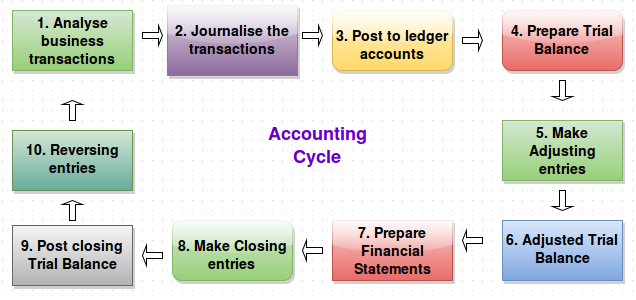

Accounting Cycle

Accounting Cycle

No comments:

Post a Comment